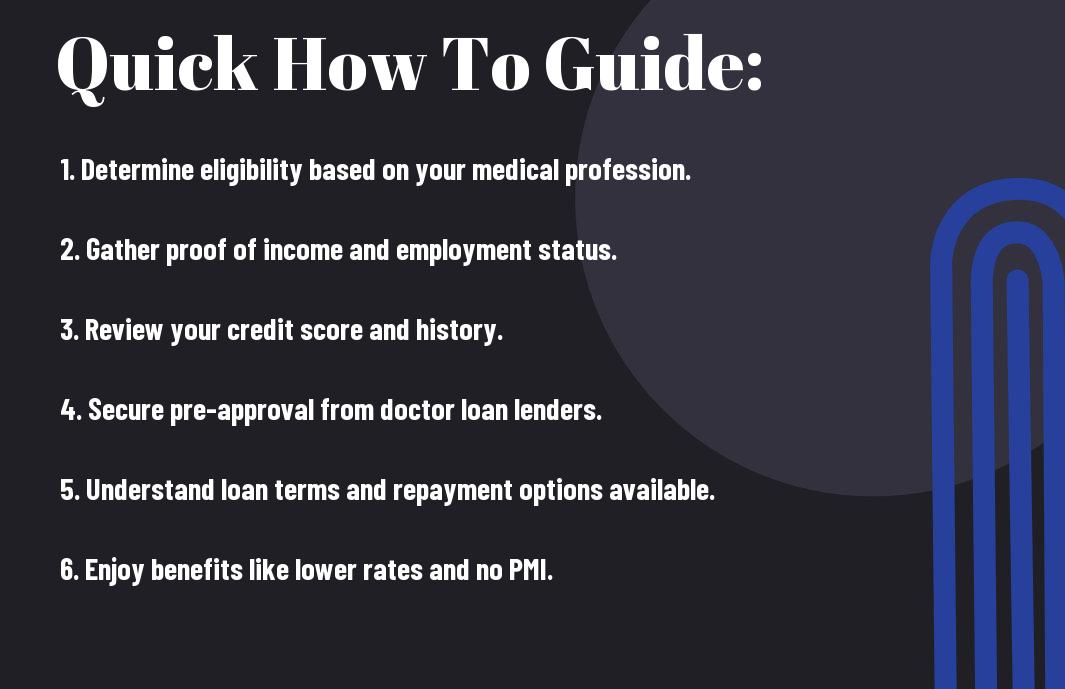

You may be considering a doctor loan as you begin on your medical career or expand your practice. These specialized loans offer unique advantages tailored for healthcare professionals, allowing you to secure favorable terms despite the financial challenges that often accompany your education and training. In this guide, we will outline the key requirements needed to qualify for a doctor loan and explore the benefits that can help you make informed financial decisions for your future.

Understanding Doctor Loans

Before venturing into the qualifications for a doctor loan, it’s necessary to understand what these loans are designed for and how they can benefit you as a medical professional. Doctor loans are specific mortgage products aimed at physicians, dentists, and other medical professionals, allowing you to secure funding for your home without the traditional barriers often faced by other homebuyers.

What is a Doctor Loan?

What sets a doctor loan apart from other mortgage options is its unique structure tailored to accommodate your financial situation as a medical professional. These loans typically offer high borrowing limits, competitive interest rates, and more flexible approval criteria, often taking into account your future earning potential rather than solely your current income.

Benefits of Doctor Loans

Loan products specifically designed for doctors come with various benefits that can significantly ease your path to homeownership. These advantages include low or no down payment options, which can help you retain more of your savings for other investments, as well as the opportunity to exclude student debt from your debt-to-income ratio when qualifying.

Understanding the benefits of doctor loans can empower you as you navigate the home-buying process. With favorable terms, you can invest in your future while minimizing the financial burden that often accompanies purchasing a property. Additionally, these loans typically come with lower closing costs and may even eliminate mortgage insurance, further enhancing your purchasing power and financial flexibility.

Key Requirements to Qualify

While qualifying for a doctor loan may seem straightforward, several key requirements must be met. Lenders typically look for proof of your medical degree, a valid medical license, and a stable employment record, demonstrating your capability to repay the loan. These criteria help ensure that you are a suitable candidate for the specialized financing options available to medical professionals.

Employment and Income Verification

An necessary step in the qualification process involves employment and income verification. Lenders will require documentation of your current job, such as an offer letter or recent pay stubs, to confirm that you have a steady, reliable income. This information helps demonstrate your financial stability and ability to manage loan payments efficiently.

Credit Score Considerations

Assuming your other qualifications are met, your credit score plays a significant role in determining your eligibility for a doctor loan. Lenders typically prefer a solid credit score, as it reflects your financial habits and reliability. However, many doctor loan programs cater to medical professionals who may have high student debt but limited credit history, ultimately providing more flexibility in qualifying.

Qualify for a doctor loan involves understanding your credit history, as lenders focus on this aspect to assess your financial responsibility. A score of 700 or higher is often ideal, but some lenders may allow for lower scores if you exhibit strong income potential and are a recent graduate. It’s vital to review your credit report before applying to identify any discrepancies that could impact your score and to make necessary improvements that can enhance your overall loan application.

Essential Documents Needed

Despite the streamlined process of obtaining a doctor loan, compiling the right documentation is critical. Lenders typically require specific paperwork that demonstrates your financial stability and professional credentials. Having these documents in order will not only expedite your application but also enhance your chances of approval for favorable loan terms.

Required Financial Documentation

You will need to provide necessary financial documents like your recent pay stubs, tax returns, and bank statements. These documents showcase your income stability and overall financial health. Additionally, if you’re in residency or fellowship, including a copy of your employment contract can help highlight your future earning potential.

Additional Paperwork

One key component of your application will be to submit various additional paperwork that supports your qualifications for the loan. This may include your medical school diploma, proof of residency or fellowship, and any licenses or certifications pertinent to your field.

For instance, lenders may also ask for a list of your current debts and any other financial obligations. Providing a comprehensive view of your financial situation aids lenders in assessing your risk profile, which is vital for securing a competitive doctor loan. Having these additional documents ready can significantly streamline the approval process and help represent you as a responsible borrower.

Tips for Improving Your Chances

Unlike conventional loans, securing a doctor loan can be competitive. To boost your chances, consider these tips:

- Enhance your credit score

- Maintain a stable income

- Limit your outstanding debts

- Gather necessary documentation early

Any proactive approach will considerably heighten your chances of approval.

Enhancing Your Credit Score

Improving your credit score is key in qualifying for a doctor loan. Start by checking your credit report for inaccuracies and disputing any errors you find. Pay down existing debts and ensure all your bills are paid on time. Even small adjustments in your credit habits can significantly impact your score over time, making you a more appealing candidate.

Preparing Financially for Application

While preparing for your application, having your financial documents organized can streamline the process. Ensure you have your tax returns, bank statements, and proof of income ready. Lenders will look for indicators of financial responsibility, so presenting a clear picture of your finances can set you apart.

Preparing financially for your application involves more than just gathering documents. Take the time to review your overall financial health, including your savings and expenses. A well-rounded financial profile can demonstrate your ability to manage future mortgage payments. This preparation can build your confidence and reduce stress when applying, making it a smoother experience overall.

Factors Influencing Doctor Loan Approval

Keep in mind that several factors can impact your doctor loan approval. These include:

- Your income and employment history

- Credit score and history

- Debt-to-income ratio

- Loan-to-value ratio

- Financial reserves

This comprehensive review helps lenders assess your ability to repay the loan.

Debt-to-Income Ratio

With a focus on your overall financial health, lenders closely examine your debt-to-income ratio (DTI). Typically, a lower DTI indicates better financial management and makes you a more attractive candidate for a doctor loan.

Loan-to-Value Ratio

The loan-to-value ratio (LTV) serves as another significant determinant in the approval process. This ratio compares the total amount of your loan to the appraised value of the property.

Plus, a favorable LTV may enhance your chances of securing better loan terms. Generally, lenders prefer an LTV of 80% or less, as it suggests lower risk. By understanding your LTV, you can better position yourself for a successful application.

Frequently Asked Questions

For those considering a doctor loan, you may have several questions regarding eligibility and the application process. This section addresses common concerns and clarifies crucial details to help you navigate your financial options effectively.

Common Inquiries

One of the most common inquiries you may have is whether you qualify for a doctor loan if you are still in residency or fellowship. Many lenders understand your unique situation and may offer loan options tailored to your financial status.

Expert Clarifications

With various lending institutions providing doctor loans, it’s vital to know the specific qualifications needed. You should look into details such as credit score requirements, debt-to-income ratios, and any available incentives that can benefit you.

This understanding will empower you to choose the best loan option for your needs. Often, lenders recognize your potential future earnings and have more flexible terms for those in the medical field. By gathering accurate information and expert insights, you can make informed decisions that suit your financial goals as a medical professional.

To wrap up

Upon reflecting, understanding how to qualify for a doctor loan can significantly enhance your financial opportunities as a medical professional. By meeting key requirements such as having a degree and managing your debt-to-income ratio, you can unlock benefits like low interest rates and no private mortgage insurance. This financial tool is tailored to support your unique situation, allowing you to focus on your career and achieve homeownership. With the right information, you can take confident steps towards securing a doctor loan that aligns with your financial goals.