Many physicians find themselves facing unique challenges when it comes to securing a mortgage. Given your specific financial situation—often characterized by significant student debt and fluctuating income—traditional lending options may not serve your best interests. Doctor loan programs are designed to address these specific needs, providing flexible terms and favorable rates. In this blog post, you will learn how these specialized mortgage products can help you navigate the complexities of home buying while maximizing your financial potential.

Understanding Doctor Loan Programs

To comprehend the intricacies of doctor loan programs, it’s vital to recognize how these unique financial products cater specifically to the needs of medical professionals. These loans are designed to make homeownership more accessible by addressing the income potential and financial challenges that may arise during the early stages of your medical career.

What Are Doctor Loan Programs?

After completing medical school, many physicians find themselves with significant student debt, which can complicate traditional mortgage applications. Doctor loan programs offer specialized financing options that take your profession into account, allowing you to qualify for home loans with favorable terms despite these financial hurdles.

Key Features and Benefits

The benefits of doctor loan programs are designed to help you secure a mortgage more easily. Key features include:

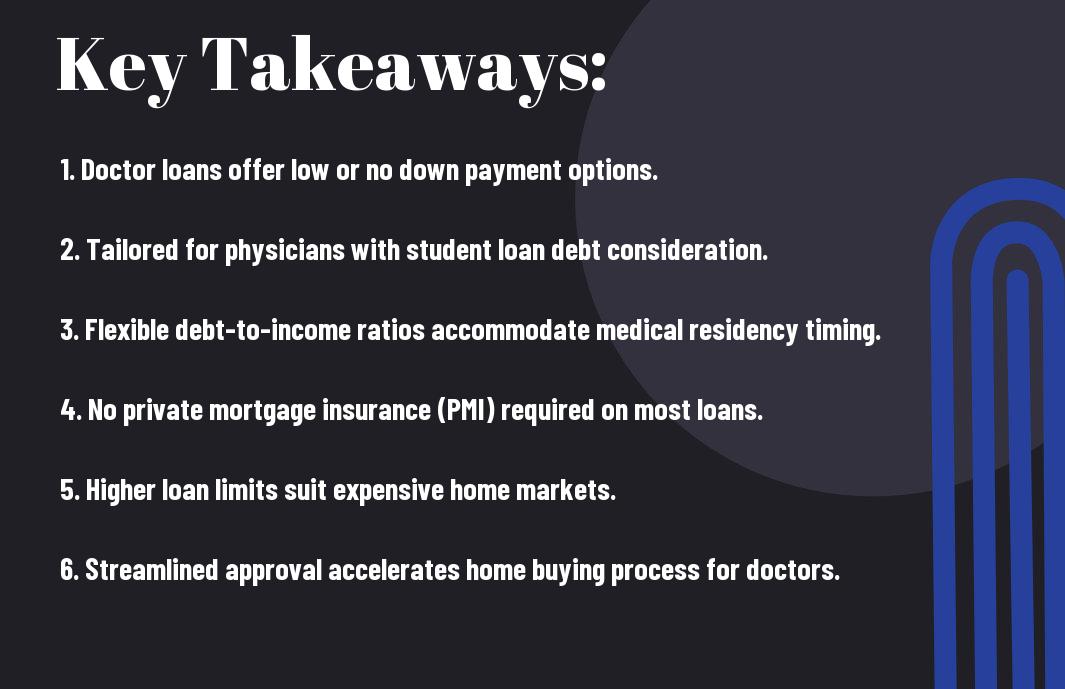

- Low or no down payment options

- No private mortgage insurance (PMI) required

- Flexible debt-to-income ratios

- Consideration of future income potential

- Loan amounts that reflect your earning capacity as a physician

Any of these benefits can empower you to achieve your goal of homeownership, even with student debt in your financial profile.

Hence, the targeted design of these programs helps address common obstacles faced by physicians. By leveraging key features such as low down payment requirements and no PMI, you can position yourself for success in securing your dream home. Additionally, these loans recognize the future earning potential that many doctors possess, making it easier for you to qualify at favorable terms.

- Possibly lower interest rates compared to conventional loans

- Quick and simplified application processes

- Options for new graduates as well as experienced physicians

Any of these features contribute to a more streamlined and supportive mortgage experience tailored specifically to your unique situation as a medical professional.

Eligibility Criteria

Some of the most important eligibility criteria for doctor loan programs revolve around your professional status, employment history, and credit score. These loans are specifically designed for physicians, making it easier for you to secure financing despite potential hurdles like student debt or limited credit history. Understanding the specific requirements can help streamline your application process and enhance your chances of approval.

Who Qualifies for Doctor Loans?

On a broad scale, doctor loans are primarily available to medical professionals such as physicians, dentists, and in some cases, residents. As a qualified physician, you typically need to provide proof of your medical degree and current employment or offer letters. Lenders often consider your specialty and income potential, which allows for favorable terms in your mortgage financing.

Common Requirements Across Lenders

One of the most common requirements across lenders for doctor loans includes a minimum credit score, usually around 700, though some may be more flexible. You may also need to provide proof of income and your medical degree, as well as documentation of your current employment. Lenders might look for a manageable debt-to-income ratio, typically not exceeding 40%, to ensure you can handle the mortgage payments alongside your other financial commitments.

Also, while requirements can vary, many lenders may ask for a down payment ranging from 0% to 10%. Your overall financial profile, including savings and existing debts, will influence the terms and rates offered. Additionally, maintaining stable employment is key; a consistent job history assures lenders of your ability to meet mortgage obligations. By familiarizing yourself with these common criteria, you can better prepare your application and secure the loan that suits your needs.

Comparison with Conventional Loans

Despite their shared purpose of financing a home, Doctor Loan Programs and conventional loans differ significantly in features that cater to physicians. Understanding these distinctions can help you make the best choice for your financial situation.

| Feature | Doctor Loan Programs |

|---|---|

| Debt-to-Income Ratio | More lenient |

| Down Payment | As low as 0%-10% |

| Loan Amount | Higher limits available |

| Mortgage Insurance | Often waived |

Interest Rates and Terms

After comparing loan types, you may find that Doctor Loan Programs generally offer competitive interest rates, tailored specifically for physicians. Lenders recognize your earning potential, which can help you secure favorable terms more easily than through conventional loans.

Down Payment Options

Among the appealing features of Doctor Loan Programs is the flexibility of down payment options. Often, these loans allow you to put down as little as 0% to 10%, making homeownership more accessible for medical professionals.

Payment preferences vary significantly depending on the lender’s guidelines and your specific financial profile. Many programs aim to alleviate the financial burdens of long medical training, allowing you to allocate funds elsewhere while still securing the home of your choice.

Advantages for Physicians

Many physician mortgage programs offer unique advantages tailored to your professional circumstances, making home ownership more attainable. These loans typically accommodate high student loan debt and often require little to no down payment, allowing you to invest in property sooner. With specialized underwriting criteria, these programs consider your future earning potential, helping you secure loans that traditional programs may deny.

Financial Flexibility

At the start of your career, financial flexibility is vital. Physician mortgage loans allow you to allocate your income towards expenses like starting a practice or funding your lifestyle, rather than locking away a significant amount for a down payment. This flexibility enables you to navigate your professional and personal finances with ease, giving you the freedom to invest in your future without significant financial strain.

Overcoming Debt-to-Income Ratios

Above all, managing debt-to-income ratios can be challenging, especially with the burden of student loans. Standard mortgage programs often disqualify you based on these ratios. However, doctor loan programs are designed with your financial profile in mind, often disregarding your student loan payments, which can significantly enhance your borrowing capacity.

The unique structure of physician loan programs allows for the exclusion of monthly student loan payments when calculating your debt-to-income ratio. This means you can qualify for a mortgage even if your overall debt level seems high. By acknowledging your potential future earnings as a physician, these programs give you the opportunity to secure a home loan that accommodates your unique financial situation, making home ownership a more realistic goal.

Potential Drawbacks

For physicians considering a doctor loan program, it’s important to be aware of potential drawbacks. While these loans offer unique benefits, they can also come with specific limitations. Understanding these drawbacks will help you make a more informed decision about your mortgage options.

Limitations and Restrictions

Between varying lender guidelines and specific eligibility criteria, doctor loan programs can come with limitations that may not fit everyone’s needs. Some lenders may only cater to particular specialties or require you to work for an approved institution, impacting your choices regarding where to live and work.

Understanding Fees and Costs

One of the critical aspects to consider is the fees and costs associated with doctor loan programs. While they often come with lower down payments or avoid private mortgage insurance (PMI), other fees may still apply, which can affect your total mortgage cost.

Even though doctor loan programs might provide advantageous terms, it’s vital to examine all associated fees and costs closely. These can include origination fees, appraisal costs, and closing costs, which can vary significantly from one lender to another. Being well-informed about these expenses will ensure that you are confident in your financial decision and fully prepared for the home buying process.

Tips for Choosing the Right Lender

Unlike traditional mortgage processes, navigating doctor loan programs requires careful selection of your lender. Consider the following tips:

- Check lender experience with physician loans

- Compare interest rates and terms

- Assess customer service and support

- Look for flexible qualifying criteria

The right lender can make a significant difference in your mortgage journey.

Researching and Comparing Options

Between the various lenders and their terms, it’s vital to weigh your options. Look at key factors such as:

Comparison Factors

| Interest Rates | Loan Terms |

| Fees and Closing Costs | Customer Reviews |

| Available Loan Programs | Qualifications Required |

Questions to Ask Potential Lenders

For a well-informed decision, ask potential lenders the right questions. This will help you gauge their experience and comfort level with your unique financial situation.

With the array of options available, be sure to ask about the specific programs they offer for physicians, any potential lender fees, as well as what documentation you’ll need to provide. Inquire about their experiences with other doctors to gain insight into how they handle physician loan applications and any unique considerations that might apply to you.

Summing up

Summing up, navigating the mortgage landscape as a physician can be streamlined through specialized doctor loan programs designed for your unique financial situation. These programs offer benefits such as lower down payments and flexible credit requirements, making homeownership more accessible for you. By understanding how these tailored options align with your professional journey, you can make informed decisions that support your goals in both your personal life and medical career. Leverage the advantages of doctor loan programs to secure the home that fits your needs.