There’s a unique pathway to homeownership designed specifically for you as a physician. Doctor mortgage loan programs offer tailored benefits that cater to your career path, financial needs, and often substantial student debt. These programs typically feature low down payment options and flexible lending criteria, enabling you to focus more on your practice and less on financial barriers. By understanding how these specialized loans work, you can make informed decisions that put you on the path to owning your dream home more efficiently.

Demystifying Doctor Mortgage Loans

Doctor mortgage loans often appear complex, but understanding them is key to leveraging their benefits. These specialized loans cater to physicians and allow you to secure financing despite potential financial hurdles. Rather than following conventional lending criteria, these loans recognize your unique career trajectory and anticipated earning potential, streamlining the path to homeownership.

Unique Features Tailored for Physicians

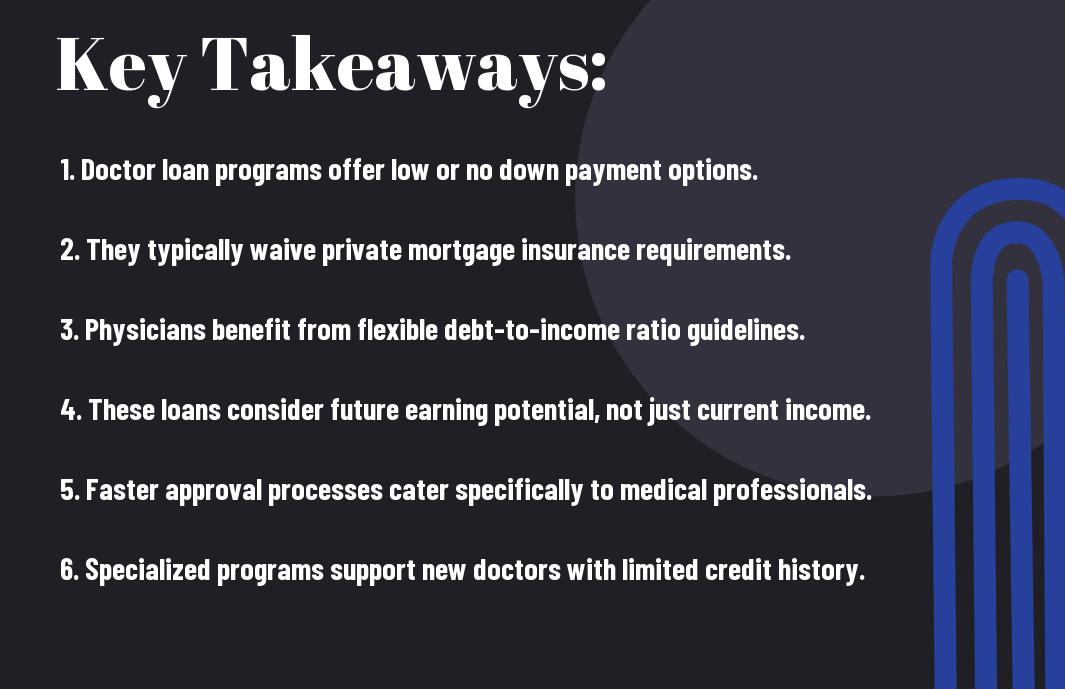

Designed with your unique financial profile in mind, doctor mortgage loans typically offer higher loan limits, reduced down payments, and more flexible credit requirements. For instance, you might find options that require as little as 0-10% down, allowing you to invest in your home without depleting your savings during the early stages of your medical career.

How These Loans Overcome Common Barriers

Doctor mortgage loans address several barriers that often hinder physicians from purchasing homes. Traditional lenders often expect a significant income history, while these specialized loans consider your future earning potential and high-demand status. Many programs are structured to minimize the impact of medical school debt, positioning you favorably in the eyes of lenders.

With medical professionals carrying substantial student debt, qualifying for a conventional mortgage can be challenging. Doctor mortgage loans counter this by factoring in your future income potential and offering flexibility with regard to DTI (debt-to-income) ratios. Instead of penalizing you for educational loans, these programs allow you to enter the housing market sooner, providing you with an opportunity to build equity as your career flourishes. This tailored approach not only eases financial strain but nurtures your homeownership aspirations, giving you a solid foundation to balance your professional and personal life effectively.

Financial Advantages in Home Purchasing

Opting for a doctor mortgage loan program can significantly impact your financial landscape when purchasing a home. From lower initial costs to favorable lending conditions, these specialized loan programs cater to the unique financial situations of physicians, helping you invest in your future with confidence.

Lower Down Payment Requirements

One of the most appealing aspects of doctor mortgage loan programs is their lower down payment requirements. Many conventional loans necessitate a minimum of 20% down, which can be daunting given the large amounts physicians often owe in student loans. In contrast, these specialized loans allow you to put down as little as 0% to 5%, enabling you to preserve more of your cash for other investments.

Competitive Interest Rates and Terms

Doctor mortgage loan programs also offer competitive interest rates and terms tailored to your needs. Many lenders recognize the high earning potential of physicians, leading them to provide favorable rates even for those without a lengthy credit history. These incentives make homeownership more attainable and affordable, significantly enhancing your financial stability.

For instance, while typical mortgage interest rates might hover around 3.5% to 4%, many physician-specific loans feature rates as low as 3% or even lower, depending on the lender and your credit profile. This difference can mean substantial savings over the life of the loan. Moreover, you can often secure fixed-rate options spanning 30 years, which means consistent monthly payments and peace of mind against fluctuating market conditions. Overall, the combination of lower rates and advantageous repayment terms empowers you to confidently move forward with your home purchase.

Navigating the Application Process

The application process for a doctor mortgage loan can differ from traditional home loans, requiring you to be well-prepared. Generally, lenders are not only interested in your financial status but also your professional standing and future earnings potential. Being organized and informed will streamline this experience, making it less daunting.

Essential Documentation and Eligibility Criteria

Your application will necessitate specific documentation that underpins your eligibility. Common requirements include proof of your medical degree, an employment contract detailing your salary, and your last two years of tax returns or W-2 forms. Familiarizing yourself with these documents ahead of time can expedite the approval process.

Tips for a Smooth Loan Approval Journey

To enhance your chances of a swift loan approval, adopt proactive strategies. Ensure all documentation is complete and up-to-date, maintain open lines of communication with your lender, and be ready to answer any questions or provide additional information promptly. This attention to detail reflects your professionalism and can significantly accelerate the process.

- Keep your financial documents organized and accessible.

- Gather references if necessary or required by your lender.

- Clarify any uncertainties with your lender to avoid confusion.

- Stay engaged throughout the process for timely updates.

- This will make the experience smoother and less stressful.

Additionally, anticipate potential roadblocks by addressing common issues in advance. Thoroughly reviewing your credit report and ensuring your credit score meets lender requirements can save significant time. Consider consulting with a mortgage professional who specializes in physician loans to gain insights tailored to your situation. Having a dedicated expert can guide you through each step, making the entire process more efficient.

- Schedule a pre-approval before house hunting.

- Limit other loan applications to avoid lender concerns.

- Maintain stable employment to reassure lenders about your income.

- Provide additional documentation if asked by your lender.

- This will bolster your application and show your commitment.

Real-World Implications of Homeownership for Physicians

Becoming a homeowner offers numerous implications for physicians beyond mere shelter. Owning a home plays a vital role in your overall sense of stability, which can positively affect both your personal and professional life. It allows you to put down roots in a community, fostering relationships and connections that can enhance your practice and improve your quality of life. Moreover, investing in a property often leads to increased financial security and opportunities for wealth-building, making it an imperative aspect of your long-term career strategy.

The Impact of Stable Housing on Career Longevity

Stable housing creates a foundation that can enhance your career longevity. With the pressure of relocation significantly reduced, you can fully focus on your practice and professional development. Establishing your home in a specific area allows you to nurture relationships with patients and colleagues, furthering your career growth and job satisfaction. In addition, reduced stress from housing instability contributes to better mental health, improving both your performance and job retention in a demanding profession.

Building Equity: A Strategic Financial Move

Building equity in your home is not just a byproduct of ownership; it’s a powerful financial strategy. As you make mortgage payments, your ownership stake in the property grows, creating a valuable asset that can appreciate over time. This equity can be leveraged in the future for other investments or financial needs. For example, selling a home after years of appreciation can yield significant returns that bolster your retirement savings or fund your children’s education. In this way, your home becomes an imperative part of your overall financial portfolio.

Investments in real estate commonly yield a solid return. On average, home values appreciate roughly 3-5% annually, depending on the market. For physicians, this growth can translate into substantial equity over time. If you purchase a home for $400,000 and it appreciates at 4% annually, within ten years, its value could rise to around $592,000. The equity you build not only acts as a financial safety net but also allows you to strategically tap into home equity lines of credit, giving you liquidity for various opportunities—from funding further education to starting a practice. Such a strategic move enhances your financial portfolio while offering versatility in managing your career and lifestyle needs.

Common Misconceptions About Doctor Mortgage Loans

Many misconceptions surround doctor mortgage loans, leading potential borrowers to overlook their potential benefits. By addressing the myths and clarifying the realities, you can better understand how these programs can work for you. Common myths include beliefs about affordability, access, and the exclusivity of these loans to certain medical professionals, which are often overstated or simply incorrect.

Debunking Myths: Affordability and Access

A prevalent misconception is that doctor mortgage loans are only for high-income earners or those with impeccable credit scores. In reality, many loan programs cater to physicians who may still be early in their careers, allowing for lower down payments and flexible credit requirements. This inclusivity means that even those with substantial student debt can find accessible pathways to homeownership.

Clarifying “Doctor Only” Labels and Inclusivity

The term “doctor mortgage loans” can create confusion, suggesting exclusivity that may discourage other medical professionals from exploring these options. In fact, many programs are designed to accommodate a variety of healthcare roles, including dentists, veterinarians, nurses, and pharmacists. Knowing the full scope of these programs expands your opportunities for securing favorable financing.

Some lenders actively promote these loans to a broader audience, recognizing the unique financial situations faced by various healthcare professionals. For example, while “doctor mortgage loans” might seem tailored exclusively for physicians, programs often include advanced practitioners like nurse practitioners or physician assistants. This inclusivity enables a wider range of individuals in the medical field to access beneficial loan terms, reinforcing the notion that homeownership is an attainable goal for many within the healthcare industry.

Conclusion

Now that you understand the numerous advantages of doctor mortgage loan programs, you can navigate the path to homeownership with confidence. These specialized loans cater specifically to your unique financial circumstances, allowing you to secure a home without the burden of traditional financing limitations. By taking advantage of these tailored solutions, you can focus on your medical career while building equity in your own home. Empower yourself with this knowledge and make informed decisions as you begin on your journey towards homeownership.